The Design

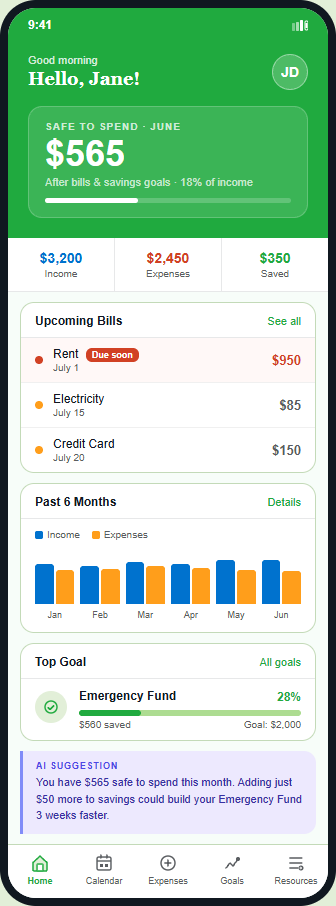

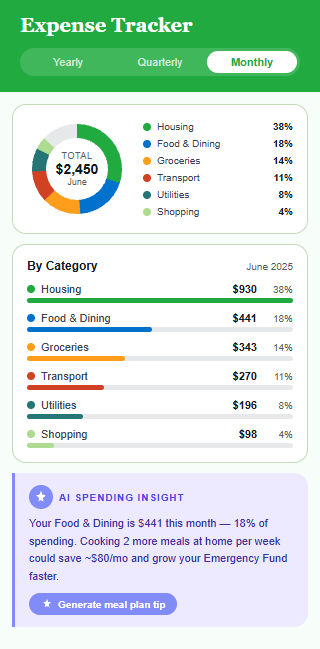

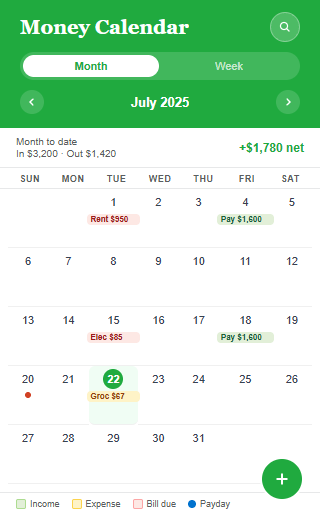

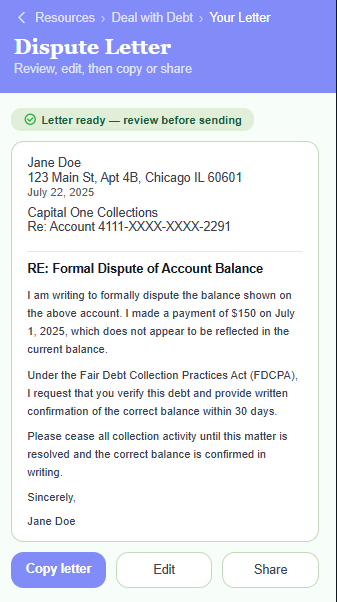

Key screens

Each screen maps to one of the three product pillars.

A consumer-facing financial empowerment app grounded in user research, designed to move vulnerable adults from reactive crisis management to proactive financial control.

My Contribution

The Problem

CFPB survey data, market research, and direct consumer and professional interviews converged on the same problem: a significant portion of U.S. adults lack both day-to-day financial control and the capacity to absorb unexpected shocks. Adults who couldn't raise $2,000 in 30 days scored just 39 on the CFPB's well-being scale, a 23-point gap from those who could. Those with under $250 in liquid savings scored 41, versus 68 for those with $75,000 or more: the largest differential in the study.

No consumer-ready tool addressed this gap. The CFPB's evidence-based resources are built for professionals: social workers, nonprofit counselors, community workers. Consumer interviews added a second barrier: among financially vulnerable populations, trust in digital financial tools is profoundly low, with concerns around privacy, bias, and hidden incentives limiting adoption. A product that users won't open cannot help them.

Research Grounding

The CFPB's national survey of over 6,000 U.S. adults provided a rigorous foundation. Three findings directly shaped MoneySmart's design priorities:

Consumer and professional interviews added the qualitative layer: people struggle not because they lack financial knowledge, but because no tool meets them in the moment of the decision not after the overdraft, not in a counseling session, but right now, when they're deciding whether to pay a bill or buy groceries.

Design Approach

The guiding discipline throughout: teach people to fish, not fish for them. Every pillar was scoped to build financial skill and confidence, not prescribe actions. Each responds directly to a barrier identified in the research and was mandated as a non-negotiable product principle from the outset.

Most finance apps show you what you already spent. MoneySmart answers the question people actually need answered: "What can I safely spend right now?" by calculating true discretionary income after upcoming bills and savings goals are accounted for. Proactive framing over retroactive reporting.

Passive financial education doesn't work. MoneySmart embeds skill-building in the context of the user's specific challenge: struggling with bills: the app guides you through prioritization; managing debt: it builds a structured repayment view. The education happens in the act of using the tool, not before it.

I mandated a zero-trust privacy architecture as a foundational pillar, not an afterthought. All financial data processing occurs on the user's device. Zero PII collected. No data sold. No upsells. "Impartial & Private by Design" is the core brand promise, and the thing no ad-supported competitor can replicate.

Usability Testing & Iteration

Two rounds of usability testing with target users validated core assumptions while exposing critical gaps in clarity and trust. Round 1 revealed confusion around safe-to-spend calculations and low confidence in privacy claims — iterations simplified the model, made the logic transparent, and reinforced "Impartial & Private by Design" through explicit UX cues. Round 2 showed improved comprehension but surfaced decision friction; contextual guidance and just-in-time prompts were introduced to support users in the moment without prescribing outcomes.

The Design

Each screen maps to one of the three product pillars.

Outcome

The product demonstrates that the adoption barrier for financially vulnerable consumers is not technological: it's trust. When a tool is genuinely impartial, genuinely private, and free of upsells, the population most resistant to commercial financial apps becomes reachable without surrendering their data or their dignity to do so.

Strategic Impact

Established a replicable model for advancing the CFPB's core mandate through effective financial education delivered directly to consumers at the moment of need.

Product Differentiation

"Impartial & Private by Design" became a defensible product moat, one no ad-supported or data-monetizing competitor can match. In a market crowded with financial apps, MoneySmart's architecture is its competitive advantage.